Our Projects

Own Your Dream Now! 3 BHKs in Kokapet | Ready to move | Premium Lake Facing Apartments

Live Where You Work | Spacious 3 BHKs in the Heart of the Financial District | From ₹2.25 Cr .

Exclusive 3BHKs | Experience the city’s rhythm in Financial District | Starting at 2.5 Crs

First-Time Home Buyer’s Guide to Hyderabad (2026): Steps, Costs & Locality Guide

Buying your first house is a significant financial decision. In Hyderabad’s real estate sector, this process is not only multi dimensional but also features numerous choices in terms of loan eligibility, neighbourhood timing, legal verification, and possession logistics. Amidst advice from family members, brokers, and forwarded WhatsApp messages, it’s common to feel overwhelmed by the questions.

The guide covers the whole journey, from the time of budgeting to the time of taking possession.From what to look around on a site visit, to which documents are important before signing to post possession.

- 1 Step 1: Define Your Budget and Assess Home Loan Eligibility

- 2 Step 2: Choose the Locality in Hyderabad that Right for You

- 3 Step 3: Shortlist RERA-Registered Projects and Visit Sites

- 3.1 Every project dealing in selling in Telangana state is required to be registered under RERA. This is your first layer of validation.

- 3.2 RERA verification of any project in Telangana: a quick guide

- 3.3 Visit rera.telangana.gov.in and search by project name or RERA number of the project present on brochures or search online.

- 3.4 On the project page on RERA, verify:

- 3.5 If a project is not RERA-registered, do not buy. No exceptions

- 3.6 What to look for on a site visit

- 4 Step 4: Legal Due Diligence. 10 Documents to Check

- 5 Step 5: Negotiate, Book, and Sign the Sale Agreement

- 6 Step 6: Home Loan Processing and Disbursement

- 7 Step 7: Registration, Possession, and Post-Purchase Tasks

- 8 First-Time Buyer Benefits: Tax Deductions and PMAY Eligibility

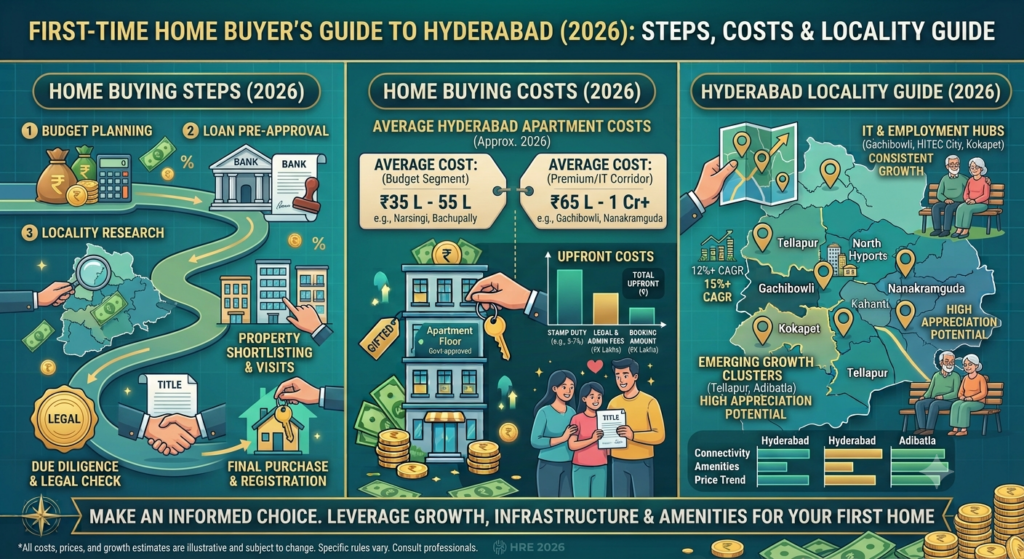

Step 1: Define Your Budget and Assess Home Loan Eligibility

Your budget is the baseline. It’s not how much you qualify for; it’s how much makes sense for your income, expenses and risk tolerance.

How to set your budget:

Begin with your net monthly salary. Banks generally expect your EMI to be less than 40–50% of your salary.

Example:If your monthly income is ₹75,000, you should be able to comfortably get an EMI of ₹30,000-37,500. At the prevailing interest rates (8.5–9.2% currently), this would allow you to take a loan of ₹50-60 lakh.

Banks generally asks you to pay 20% of the property price from your own as down payment before they give the loan.So,if you have Rs.15 lakh saved, Rs.50 lakh you get as loan, Rs.65 lakh is you total budgetbudget.

What Rs. 50L, Rs. 90L, and Rs. 2 Cr+ can buy you in Hyderabad today:

Rs.65-90 lakh : 2 BHKs, 900-1,300 sq. ft., in upcoming corridors like Bachupally, Kompally or Tellapur. Ideal for buyers looking for flats with lower entry cost but with a decent level of connectivity to IT hubs.

Rs.1-2.2 crore : It can get you a 2-3 BHK in main corridors like Gachibowli,Financial District and Kokapet. They have metro connectivity, good infrastructure, and good rental demand.(Source)

Home loan eligibility checklist

Before you approach a lender, verify:

1) Age: Most banks accept applicants aged 21–65 at the time of loan disbursal.

2) Employment: Permanent roles or self-employment with 2+ years of audited accounts.

3) Income stability: Last 2–3 years salary slips and Form 16s (salaried) or ITRs (self-employed).

4) CIBIL score: Typically 750+. Check your score free at CIBIL.com.

5) Debt-to-income ratio: Existing EMIs + new home loan EMI should be less than 50% of net income.

6) Co-applicant: Spouse or Parent. Co-applicants, usually a spouse or parent, can be added to enhance eligibility if they have a more stable income.

Pre-approval: the smart move

Get a pre-approval letter from your choice bank, it takes 3-5 working days and requires only basic documents. That will help you know your budget for projects and localities you can target.

Step 2: Choose the Locality in Hyderabad that Right for You

Not every growing area is right for every buyer. Your choice should match your job location, family needs, and investment horizon.

Locality match table: buyer profile to neighbourhood

| Buyer profile | Best localities | Why | Typical budget |

| IT professional, single or couple, renting now | Gachibowli, Kondapur, Miyapur, Financial District | Close to offices, high rental demand, metro-connected | ₹75L–1.2 Cr |

| Family with school-age children | Jubilee Hills, Banjara Hills, Manikonda, Narsingi | Good school catchments, parks, quieter roads, community feel | ₹1 Cr+ |

| Young couple, budget-conscious | Bachupally, Kompally, Bowenpally | Affordable, improving infra, growing job hub presence | ₹45–75L |

| Senior couple or investor prioritizing stability | Gachibowli, Kondapur, Nanakramguda | Established markets, low vacancy, strong resale | ₹75L–1.2 Cr |

| Investor seeking value growth | Tellapur, Mokila, emerging SRDP corridors | Supply-constrained, upcoming infra, long-term upside | ₹60–1 Cr |

Questions to ask before choosing a locality

Who actually wants to live here right now? If a locality has strong job hub proximity (IT, pharma, manufacturing), rental demand is typically steady. If it’s purely on “future potential”, occupancy rates may be low, and your flat could sit vacant or rent for less than expected.

How good is connectivity? Calculate commute time from the flat to your office during peak traffic hours. Use Google Maps and give yourself a 5–10 minute buffer. If schools are on your radar, verify their location and whether they match your child’s academic year.

What does the supply pipeline look like in the next 5–10 years? Check HMDA approvals and project launches planned in the locality. If 50+ new projects are launching, prices may plateau.If supply is limited, appreciation will higher due to demand.

Step 3: Shortlist RERA-Registered Projects and Visit Sites

Every project dealing in selling in Telangana state is required to be registered under RERA. This is your first layer of validation.

RERA verification of any project in Telangana: a quick guide

Visit rera.telangana.gov.in and search by project name or RERA number of the project present on brochures or search online.

On the project page on RERA, verify:

- Registration status: Should be “Registered”, not “Suspended” or “Under Review”.

- Approved floor plan: Confirm that floor plan is the one that the builder is marketing. This has occurred very rarely, but has happened.

- Approved area & configuration: Verify if carpet area (useable area), built-up area and super built-up area as advertised matches with RERA filing.

- Timeline: Note the promised possession date and any delays already flagged in update statements.

- Escrow compliance: Seller accounts reflect if builder funds are held in escrow accounts (bank supervised), a safety feature for buyers.

If a project is not RERA-registered, do not buy. No exceptions

What to look for on a site visit

Construction stage: Is the structure sound? Check for water seepage, cracks, or poor shuttering finish. (MIVAN shuttering typically yields better floor-to-ceiling heights and finish quality compared to conventional methods, if that matters to you.)

Common areas: Visit the amenity spaces (gym, clubhouse, parking) to get a feel for actual quality vs. brochure renderings.

Surroundings: Walk around the project boundary. Check for encroachments, water logging during monsoons, or proximity to waste dumps or industrial units.

Site office staff: Ask specific questions about possession timeline, payment schedules, and escalation policies. Professional, clear answers are a good sign.

Exit routes: Verify vehicle access to the main road. A project bottlenecked by a single narrow lane can feel cramped.

Step 4: Legal Due Diligence. 10 Documents to Check

Before executing a sale agreement, your lawyer (or legal consultant) should confirm the validity of these 10 documents. This is typically a ₹5,000–10,000 exercise that can protect you from title disputes, encumbrances or other hidden liabilities.

The 10-point legal checklist:

1.Title Deed / Sale Deed of the Land: Ensure the builder has clear ownership of the land. Confirm the chain of ownership for at least the past 12 years.

2.Encumbrance Certificate (EC): A public document evidencing the fact that the property is not mortgaged or encumbered by way of a mortgage, loan or any legal suit, etc. It should be clear or with only bank mortgages pertaining to the project only ( which get discharged at possession).

3.Approved Site Plan/Layout by HMDA or GHMC. Ensure that the Footprint, setbacks, and density of the building corresponds to the Approval.

4.Municipal Approval and Occupancy Certificate (OC) / Commencement Certificate (CC): The project should have CC. OC comes after construction is complete, typically just before or shortly after possession.

5.RERA Registration Certificate: As covered above, with active status.

6.Building Bylaws and Copy of the Approved Plan: Establishes that building is in sync with Telangana’s construction norms on aspects such as FSI (Floor Space Index), parking ratio, setbacks, etc.

7.No Objection Certificate (NOC) from Municipal Corporation (GHMC/HMDA): This certifies that the property has no pending property taxes, no violations and has no objections for the proposed development.

8.Structural Stability Certificate (SSC) / Geological Report: In lieu of an SSC, developers may submit geological surveys that demonstrate that the soil in the area is stable. This is sometimes acceptable for developments on particular lands/zones that are known to be sensitive.

9.Fire Safety and IFCO Compliance Certificate : The project should be approved by the Fire Department and Telangana State Housing Board or similar organization.

10.GST Registration and Compliance Certificate: Check that the builder is GST registered and compliant for sales as it impacts your tax liability. If any of these are missing or unclear, ask the builder or lawyer to explain before you proceed.

Step 5: Negotiate, Book, and Sign the Sale Agreement

Once you’ve chosen a project and verified legal documents, it’s time to negotiate and formalize the purchase.

Negotiation basics

Builders in Hyderabad have some flexibility, especially on:

- Booking discount: First 10–20 units in a phase may have 2–5% discounts.

- Payment schedule: You can sometimes negotiate extended payment timelines, reducing upfront burden.

- Inclusions: Free car park, upgraded flooring, or kitchen appliances may be negotiable.

- GST: In rare cases, builders absorb GST for qualified buyers; more often, it’s additional.

Do not expect deep discounts on premium locations. Builders hold firm on price in areas with strong demand.

Booking amount and payment schedule

Typical booking structures:

- Booking amount: 5–10% of the property value, paid to the builder (sometimes held in escrow).

- Construction-linked payments: Additional installments tied to construction milestones (foundation, structure, finishing, pre-possession).

- Final payment: 10–20% due on or just before possession, after loan disbursement.

Ask for a transparent payment schedule in writing before you sign the agreement.

The sale agreement: what to review

The sale agreement is a legal contract between you and the builder. Key clauses to review with your lawyer:

- Property description: Exact flat number, floor, carpet area, built-up area, parking details.

- Sale price and payment terms: Total consideration, payment milestone dates, and consequences of default.

- Possession clause: Target date, grace period, and penalties for delay (usually ₹X per day or per month).

- Force majeure: Unforeseen events (war, natural disaster) that may delay possession; clarity on your remedies.

- GST clause: Who bears GST if applicable, and how it’s calculated.

- Stamp duty and registration: Usually buyer’s responsibility; confirm in the agreement.

- Maintenance charges and corpus fund: Post-possession obligations and how they’re calculated.

Do not sign until you’ve read and understood every clause. Amendments are possible before signing but difficult after.

Step 6: Home Loan Processing and Disbursement

After booking, apply for your home loan at your chosen bank or NBFC. The loan processing typically takes 4-6 weeks.

Documents you’ll need for loan processing

- Last 2–3 years of salary slips and annual Form 16 (salaried) or audited ITRs (self-employed).

- Bank statements for 6–12 months.

- Identity proof, address proof, and PAN card.

- Sale agreement and property documents.

- Project’s RERA certificate and approval documents.

- Credit report (CIBIL).

The loan process timeline

- Application and document submission: 2–3 days.

- Bank’s in-house verification: 7–10 days. The bank confirms your employment, income, and CIBIL score.

- Property valuation: 5–7 days. The bank sends a valuer to inspect the property and confirm its market value.

- Credit sanction: 3–5 days. If everything checks out, the bank issues a sanction letter with the loan amount and interest rate.

- Legal verification (by bank’s lawyer): 7–10 days. The bank’s legal team verifies the property title and sale agreement.

- Loan approval and disbursal: 3–5 days after legal clearance.

Total: 4–6 weeks from application to first disbursement.

Disbursement: how it works

Banks typically disburse in tranches tied to construction progress:

- First disbursement (40% of sanctioned loan): Upon booking and sale agreement.

- Subsequent disbursements (30–40% each): As construction reaches agreed milestones (structure, finishing, pre-possession).

- Final disbursement (remaining amount): At possession, after RERA mutual agreement and builder’s submission of occupancy certificate.

You’ll receive disbursement confirmation letters; share these with your builder for payment reconciliation.

Step 7: Registration, Possession, and Post-Purchase Tasks

Possession day is the official day when you take over the flat. But there’s still some work to do after that.

Before you take possession: the final checklist

- Ask for the occupancy certificate (OC): This has to be provided by the builder. It certifies that the building is complete and safe.

- Final disbursement of home loan: Fix with the bank for disbursal of balance loan amount by the date of possession.

- Date for possession inspection: Do walk through with builder and one other person.

- Look for leaks, water penetration, paint finish and appliance operation.

- Verify utility connections: Check that water, electricity, and sewer lines are active and functional.

- Get possession documents: Take copies of the OC, final bill of sale, and common area details.

Post-possession tasks: the 6-month window

1. Property registration and mutation (₹10,000–20,000): Register the sale deed with the Sub-Registrar’s office. This is your legal proof of ownership. Timeline: 15–30 days after possession. Do not delay; it strengthens your title.

2. Khata transfer (₹3,000–5,000): Update your name in the municipal property records. Contact your GHMC ward office. This is necessary for paying property taxes and accessing municipal services.

3. IFMS / Property tax registration: Register with IFMS (Integrated Financial Management System) or your municipal authority to pay property taxes. Annual tax is typically 5–8% of the property’s registered value.

4. Corpus fund contribution: Pay your share of the corpus fund (building maintenance fund) to the resident welfare association. Usually ₹50–150 per sq. ft. depending on the project.

5. First maintenance charges

6. NOC from municipal corporation: Obtain a No Objection Certificate confirming no property taxes or violations are pending. Needed for future resale.

First-Time Buyer Benefits: Tax Deductions and PMAY Eligibility

The government offers tangible financial support for first-time home buyers.

Income tax deductions under the Income Tax Act

Section 80C (principal repayment): You can claim up to ₹1.5 lakh per financial year as a deduction on the principal component of your home loan EMI. This reduces your taxable income directly.

Example: If your annual principal repayment is ₹2 lakh, you can deduct ₹1.5 lakh in that year. The remaining ₹0.5 lakh carries forward to the next year.

Section 24(b) (home loan interest): Deduct up to ₹2 lakh per financial year on the interest portion of your EMI. Unlike Section 80C, this deduction is ongoing; you can claim it for the entire duration of the loan (20–30 years).

Section 80EE (additional interest deduction): If you bought your first home before March 31, 2017, and your home loan is ₹50 lakh or less, you could claim an additional ₹50,000 per year as a deduction on interest. (This scheme has been discontinued for purchases from April 2017 onwards, but existing beneficiaries can still claim.)

Section 80-IB / 80-IA (for developer deductions): Some developers offer tax-backed schemes. Verify with your chartered accountant (CA) if your project qualifies.

Pradhan Mantri Awas Yojana (PMAY)

PMAY offers central government subsidies for first-time home buyers earning up to ₹18 lakh annually (₹27 lakh for larger units in certain cities).

Subsidy amount: ₹2.67–4.67 lakh depending on income bracket and loan amount.

Eligibility:

- First-time buyer.

- Self-occupied property (not rental or investment).

- Property value up to ₹45 lakh (₹60 lakh in metros).

- Income within prescribed limits.

Check pmayuclap.gov.in to verify eligibility for your income and preferred locality.

In Hyderabad, PMAY benefits are limited to certain GHMC-approved sites and affordable housing projects. Many modern residential projects in established corridors do not qualify, so verify before applying.

Stamp duty concessions

Telangana offers reduced stamp duty for first-time home buyers:

- Standard stamp duty: 4% of the property value.

- First-time buyer concession: Typically reduced to 3–3.5% in some taluks. Verify current rates with your Sub-Registrar’s office.

Registration fees are separate (0.5% on average) and are not concessional.

FAQs

Q1: What is the step-by-step process to buy a home in Hyderabad?

A: The process involves seven key steps: (1) Define your budget and get home loan pre-approval, (2) Choose a locality that matches your job and family needs, (3) Shortlist RERA-registered projects and verify legal documents, (4) Conduct legal due diligence on the property and project, (5) Negotiate, book, and sign the sale agreement, (6) Complete home loan processing and secure disbursement, and (7) Take possession and complete post-purchase registration and mutation tasks.

Q2: What budget do I need to buy a first home in Hyderabad in 2025–2026?

A: It depends on your locality and preferences. A 2 BHK in budget-friendly corridors like Bachupally or Kompally ranges from ₹45–75 lakh. Established IT hubs like Gachibowli or Kondapur range from ₹75 lakh to ₹1.2 crore for 2–3 BHK configurations. Premium micro-markets like Kokapet or HITEC City start at ₹1.2 crore and go higher. Factor in an additional 8–12% for stamp duty, registration, and possession costs beyond the base flat price.

Q3: How do I get a home loan as a first-time buyer in Hyderabad?

A: Approach your bank or NBFC with salary slips, Form 16 or ITRs, bank statements, and identity proof. Most banks allow loan-to-value (LTV) of up to 80%, meaning you’ll need a 20% down payment. Pre-approval takes 3–5 days. Full loan processing (including property valuation and legal verification) takes 4–6 weeks. Apply early so your pre-approval gives you a clear budget to work within.

Q4: What are the tax benefits available to first-time home buyers in India?

A: You can claim (1) up to ₹1.5 lakh per year under Section 80C for principal repayment, (2) up to ₹2 lakh per year under Section 24(b) for home loan interest, and (3) potentially an additional ₹50,000 under Section 80EE if eligible. Beyond income tax, you may qualify for a Pradhan Mantri Awas Yojana (PMAY) subsidy of ₹2.67–4.67 lakh if your income is under ₹18 lakh and your property is self-occupied. Verify PMAY eligibility with your lender, as not all Hyderabad projects qualify.

Q5: Which areas in Hyderabad are best for buying a first home?

A: It depends on your priorities. For IT professionals with strong rental demand and metro connectivity, Gachibowli, Kondapur, Miyapur, and the Financial District are solid choices in the ₹75L–1.2 Cr range. For budget-conscious first-time buyers, Bachupally, Kompally, and Bowenpally offer 2 BHKs from ₹45–75 lakh with improving connectivity. For families prioritizing schools and quieter surroundings, Manikonda, Narsingi, and Jubilee Hills are worth exploring at higher budgets. For long-term value, emerging corridors like Tellapur and Mokila offer supply-constrained growth potential.

Q6: What documents should I check before buying a flat in Hyderabad?

A: Ensure your lawyer verifies the title deed, encumbrance certificate, RERA registration, sanctioned layout, occupancy certificate or commencement certificate, municipal NOC, building bylaws, fire safety certificate, IFCO compliance, and GST registration. These 10 documents protect you from title disputes, encumbrances, and hidden liabilities. The verification typically costs ₹5,000–10,000 and takes 7–10 days.

Q7: How do I verify a RERA-registered project in Telangana?

A: Visit rera.telangana.gov.in, search by project name or RERA registration number, and verify that the project shows “Active” or “Registered” status. Cross-check the sanctioned layout, carpet area, built-up area, approved configuration, promised possession date, and escrow account details against what the builder is advertising. If a project is not RERA-registered, do not buy under any circumstances.

Q8: What costs are involved beyond the flat price when buying in Hyderabad?

A: Beyond the base flat price, budget for stamp duty (4%, occasionally 3–3.5% for first-time buyers), registration charges (0.5%), GST if applicable (5% for under-construction properties), home loan processing fees (0.25–0.5%), IFMS or municipal registration (₹1,000–2,000), corpus fund (₹50–150 per sq. ft.), and possession-related costs like inspection and documentation (₹10,000–20,000). Total additional costs typically add 8–12% to the base flat price. Plan accordingly in your budget.

Own Your Dream Now! 3 BHKs in Kokapet | Ready to move | Premium Lake Facing Apartments

Live Where You Work | Spacious 3 BHKs in the Heart of the Financial District | From ₹2.25 Cr .

Exclusive 3BHKs | Experience the city’s rhythm in Financial District | Starting at 2.5 Crs