Encumbrance Certificate in Telangana: Online Process, Fees & What to Check

Every year in Telangana property buyers pay registration charges only to discover later that the seller had an undischarged home loan against the property. An Encumbrance Certificate pulled before signing the agreement would have shown that mortgage.

Let us first understand a few basics and then dive deeper.

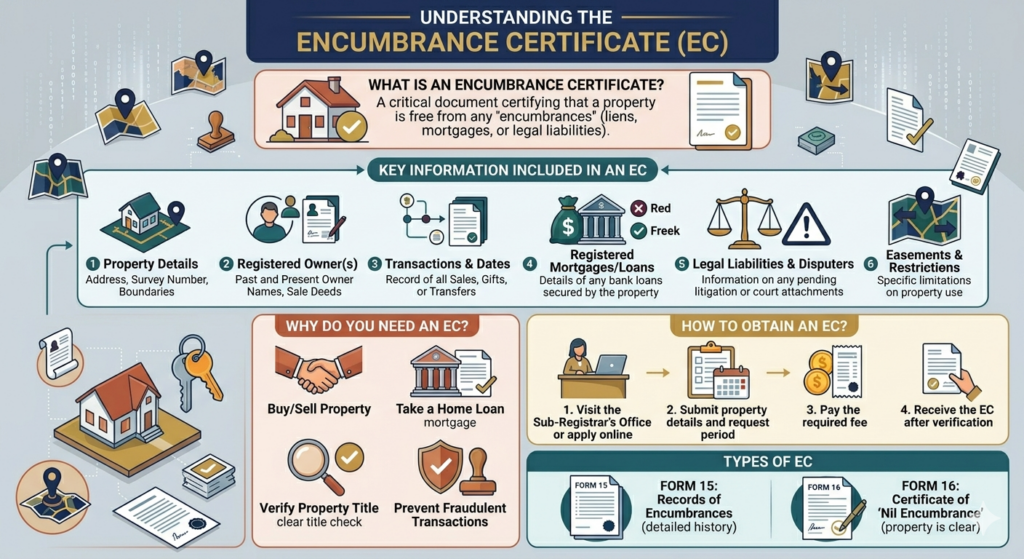

1.What Is an Encumbrance Certificate?

An Encumbrance Certificate is a document. It lists every registered transaction involving a property over a specified period. In Telangana these records are maintained by the Inspector General of Registration and Stamps (IGRS).

The word “encumbrance” refers to any charge, lien or liability attached to a property. Common encumbrances include:

* An existing home,Mortgage

* A sale deed registered in someone Name

* A gift deed transferring the property

* A court order, attachment or injunction

* A lease agreement registered over the property

2.Why Is an EC Critical Before Buying Property in Telangana?

The Encumbrance Certificate answers the one question every property buyer must resolve before committing funds: is this property legally available for sale?

Without an Encumbrance Certificate check a buyer has no way of knowing whether:

* The seller has a home loan against the property

* The same property was already sold to someone and the sale was registered

* A court has attached the property as part of a dispute

3.Encumbrance Certificate Application Process

Online Process:

* Go to registration.telangana.gov.in

* Navigate to Services then select Encumbrance Certificate

* Enter property details

* Enter the search period

* Fill details

* Review and pay

*. Receive acknowledgment

* Download the Encumbrance Certificate

Offline Process

* Visit the Sub-Registrar Office

* Obtain Form 22

* Fill in property details

* Submit with your identity proof and the applicable fee

* Collect after 5-7 working days

Encumbrance Certificate Fees in Telangana

* Base Encumbrance Certificate fee (up to 1 year search): Rs. 200

* Additional fee per year beyond the first: Rs. 100 Per year

* Meeseva service charge ( route): Rs. 25-50

Example Calculations

* 1-year search: Rs. 200

* 5-Year search: Rs. 200 + (4 X Rs. 100) = Rs. 600

* 13-Year search: Rs. 200 + (12 X Rs. 100) = Rs. 1,400

* 30-Year search: Rs. 200 + (29 X Rs. 100) = Rs. 3,100

Key Takeaways

* An Encumbrance Certificate shows all registered property transactions in Telangana for a searched period

* Two forms are issued: Form 15 (transactions found) and Form 16 (NIL EC no transactions found)

* Online applications, via the IGRS Telangana portal are processed in 1-6 working days

* The fee is Rs. 200 Base plus Rs. 100 Per year searched

* Banks require an Encumbrance Certificate covering at least 13-15 years before sanctioning any home loan

For a property purchase a 13-15 year Encumbrance Certificate or EC costing Rs. 1,400-1,600 Is practice.

The cost is negligible relative to the risk it helps you manage.

4.How to Read Your EC: Section by Section

A Telangana EC typically contains the following sections:

* Header details: Property identification. Survey number, extent (area) village, mandal, district and the SRO that has jurisdiction.

* Applicant and search period: Your name, application date and the period covered by the search.

* Transaction entries (Form 15 Each registered transaction appears as a row:

* Serial number

* Date of registration

* Document number

* Parties involved (executant and claimant)

• Type of document (sale deed, mortgage deed, gift deed, lease, court decree)

• Amount of consideration

5.What to look out for while analyzing entries:

• Sale deeds: Verify the ownership chain against the information provided by the vendor.

The recent sale should name the current seller as the buyer in that entry.

* Mortgage entries: Look for any mortgage or hypothecation entries. If found confirm whether they have been discharged (a discharge entry or a release deed should appear subsequently). An outstanding mortgage means that the bank will still have a lien on the property.(Source)

* Court action: Any actions taken in court including an injunction or order is a red flag. Consult your lawyer before proceeding.

* Gift or family settlement entries: These are legitimate. Verify that no disputes are outstanding regarding the settlement.

6.Validity and How Often You Should Renew

A Telangana EC has no statutory expiry date in the way a driving licence does. However the relevance of an EC is time-bound: it reflects the registered transaction history up to the date of its issuance.

Practical validity guidelines:

* For a property purchase: an EC issued within the 6 months is generally accepted; pull a fresh one if more than 6 months have passed since your last check particularly if the sale agreement has been delayed.

* For a home loan: banks typically require an EC issued within the 3-6 months.

* For litigation or court proceedings: the court will specify the required period.

* After purchase: pull an EC within 3 months of your registration to confirm your own sale deed has appeared in the records correctly.

If you are in the middle of a property negotiation that has stretched over months a second EC pull before final payment is a reasonable precaution. Registration records are updated continuously. A new mortgage or attachment could have been registered against the property in the interval.(Source)

7.Steps When there is Some Inconsistency or Unusual Entry

Presence of an entry in an EC doesn’t necessarily imply that the property can’t be sold.It means you need to investigate before proceeding.

If the EC shows an existing mortgage or home loan

* Request the sellers for a loan sanction letter and balance amount of the outstanding loan.

* Get NOC from the bank that has issued the loan prior to signing any agreement.

* Alternatively structure the deal so that part of the sale consideration directly pays off the existing loan and the bank issues a release deed and NOC simultaneously at registration.

* If the EC shows a court attachment or injunction:

* Stop the transaction immediately. Take legal advice.

* A court order on a property means it cannot be freely sold until the court lifts the order; any sale in violation of a court order is voidable.

* If the EC shows a sale to a party (not the current seller):

* This is the most serious scenario: it means the property was registered in someone elses name.

* Do not proceed without a title search by a property lawyer covering the complete ownership chain.

* If the EC shows an entry you cannot reconcile:

* Visit the Sub-Registrars Office with the document number shown in the entry and request to inspect the registered document.

* All registered documents are record and can be examined at the SRO.

A buyer in Miyapur who discovered a mortgage from 2019 in the EC of a resale flat they were about to purchase was initially concerned the deal would fall apart. The sellers bank confirmed a balance of Rs. 14 Lakh. The purchase price was structured so that Rs. 14 Lakh was paid directly to the bank at the time of registration; the bank issued an NOC and release deed the day. The transaction completed cleanly. The EC finding did not kill the deal; it shaped how the deal was structured.

8.EC for Home Loans: What Banks Check

Every major bank in India requires an Encumbrance Certificate as part of the home loan documentation process. Here is what they are specifically verifying:

* No existing mortgage on the property: The EC must show that the property is not already pledged with another bank or financial institution. If it is the new lender requires a NOC and release deed from the existing lender before proceeding.

* ownership chain: The EC entries should be consistent with the title documents the seller provides. If the EC shows a gap in ownership or an unaccounted transfer the banks legal team will flag it.

* Search period: Most banks require a 13-15 year EC. Some banks ask for 30 years for resale properties or plots. Check your banks requirement before applying for the EC to ensure you cover the right period in one application.

* Form 15 vs Form 16: Banks are comfortable with a Form 15 EC long as all entries are consistent with the chain of title documents. A Form 16 (NIL EC) is. Sometimes prompts the banks legal officer to verify independently since a NIL EC on a property with a long ownership history can indicate missing registrations.

* Timing: Banks typically require the EC to have been issued within the 6 months preceding the loan sanction. If your EC is older you may need to apply for an one before the banks legal clearance is finalised.

For buyers who want to understand the range of protections they have as homebuyers in Telangana including what documentation a seller must legally provide and what recourse exists when documents are not in order the guide to homebuyer consumer rights in India covers the regulatory framework clearly.

For buyers considering resale flats in Hyderabad and wanting a checklist of documents to verify beyond the EC the resale flat buying guide for Hyderabad addresses each document in the due diligence chain.

9.Before you proceed with any property in Telangana

Before you proceed with any property in Telangana whether a flat resale apartment or plot run through these three EC checks:

* Has the EC been pulled for a period of at least 13 years? If a bank home loan is involved check the banks requirement.

* Have you read every entry in Form 15. Confirmed that the ownership chain matches what the seller has represented?

* If any entry is unclear (mortgage, court order or unfamiliar name) have you verified that entry at the Sub-Registrars Office before signing anything?

If all three answers are yes you have done the minimum. The EC is not the document in a property due diligence checklist but it is almost always the first one to pull.

10.FAQs

1.What is an Encumbrance Certificate?

An Encumbrance Certificate or EC is a document from the Sub-Registrars Office showing all registered transactions on a property for a specified period. These include sales, mortgages, gift deeds, leases and court orders. It confirms whether the property carries any legal liabilities from registered records. It is one of the important documents to check before any property purchase in Telangana.

2.How much does an EC cost in Telangana?

The base EC fee in Telangana is Rs. 200 For a one-year search, plus Rs. 100 For each year. A 13-year search costs Rs. 1,400. Meeseva centres add a service charge of Rs. 25-50. Portal convenience charges are minimal. Displayed at payment.

3.How long does it take to get an EC online?

Online ECs applied through the IGRS Telangana portal at registration.telangana.gov.in are typically issued within 1-6 working days depending on the year range requested and the Sub-Registrars verification workload. Offline applications via the SRO or Meeseva take 5-7 working days.

4.Is EC mandatory for a home loan?

Yes. Every bank and housing finance company in India requires a recent Encumbrance Certificate as part of the home loan documentation. Most require it to cover at the last 13-15 years. The EC is specifically used to confirm there is no existing mortgage on the property and that the ownership chain is consistent with the title documents.

5.What is a NIL Encumbrance Certificate?

A NIL EC, issued in Form 16 means the Sub-Registrars database shows no registered transactions on the property, for the searched period. While this can indicate a title it can also mean that transactions occurred but were not registered. Always supplement a NIL EC with a title deed check and revenue records verification before concluding that the property is free of encumbrances.