The Ultimate Guide to Home Loan Down Payment: Impact, Benefits & Strategies

Congratulations! You’ve decided to embark on the exciting journey of homeownership. As a potential first-time buyer, navigating the home loan process can feel overwhelming. One of the most crucial aspects to understand is the home loan down payment – the initial sum you pay upfront before securing a home loan. This guide will equip you with the knowledge to make better decisions about your down payment, helping you find your dream home with ASBL.

Understanding the Role of Down Payment in Home Loans in India

A down payment acts as a security deposit for the lender. It demonstrates your financial commitment to the property and also reduces the overall loan amount you need to borrow. Here’s a breakdown of its significance:

- Reduced Loan Amount & Lower Interest Rates: With a larger down payment, you’re essentially borrowing less from the lender. This translates to a lower loan amount, which in turn, incentivizes lenders to offer you a more competitive interest rate. This significantly impacts your monthly EMIs (Equated Monthly Instalments) and total loan cost over the years. Let’s say you’re looking at a ₹2 crore property. With a 20% down payment (₹40 lakh), your loan amount would be ₹1.6 crore. A lower interest rate on this smaller loan amount can save you lakhs of rupees over the loan term.

- Avoiding Mortgage Guarantee: In some cases, if your down payment falls below a certain threshold (often 20%), lenders may require PMI (Private Mortgage Insurance)– an additional monthly insurance premium. This insurance protects the lender in case of default, but it adds to your overall loan cost. A substantial down payment can help you avoid this additional expense.

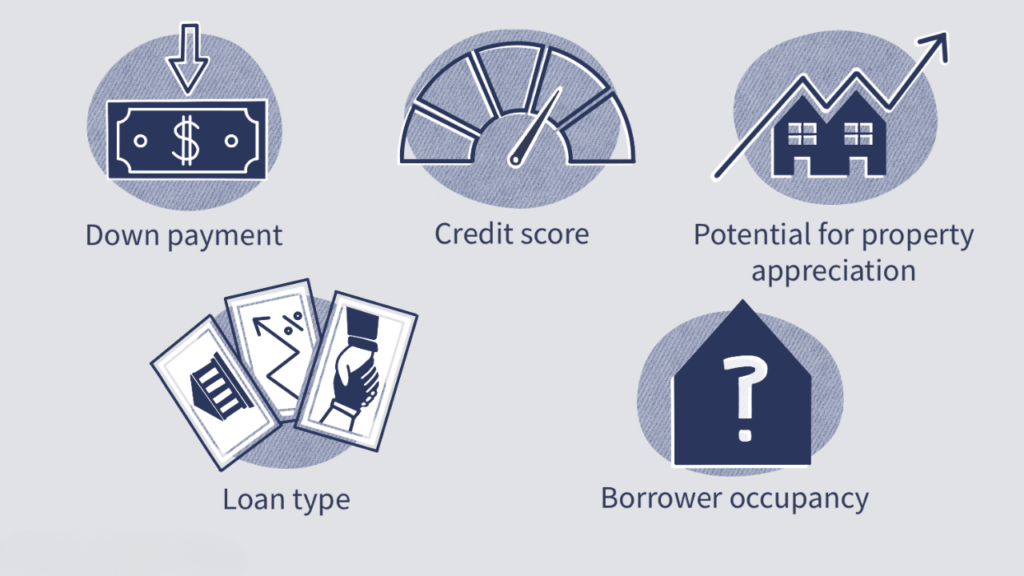

Factors Affecting Down Payment Requirements

The minimum down payment required for a home loan can vary depending on several factors:

- Loan Type: Government-backed schemes like Pradhan Mantri Awas Yojana (PMAY) may have lower down payment requirements (around 5%) compared to conventional loans offered by banks and Housing Finance Companies (HFCs), which typically require a minimum of 10% down payment.

- Credit Score: A strong credit history (CIBIL score) signifies your financial responsibility and creditworthiness. Borrowers with higher credit scores (usually above 750) may qualify for lower down payments and potentially better loan terms.

- Loan-to-value Ratio (LTV): This ratio compares your loan amount to the property value (loan amount divided by property value). A lower LTV (achieved through a larger down payment) indicates a smaller risk for the lender. For example, a 15% down payment on a ₹2 crore property would result in an LTV of 85% (₹1.7 crore loan / ₹2 crore value). Generally, lenders prefer lower LTVs as it reduces their risk

Unveil the 50-50 payment plan

Methods to Accumulate Down Payment Funds

Saving for a down payment in India requires discipline and planning. Here are some strategies you can consider:

- Budgeting and Saving: Create a realistic budget to identify areas where you can cut back on expenses. Allocate those funds towards a dedicated down payment savings account. Consider using a budgeting app or spreadsheet to track your income and expenses.

- Boosting Your Income: Explore ways to increase your income, such as taking on a freelance project or starting a small side hustle. Look for opportunities to earn extra cash without jeopardizing your current job.

- Gift Funds: Certain loan programs may allow you to use monetary gifts from close family members towards your down payment. You can check with potential lenders about their specific eligibility requirements for using gift funds.

- Government Subsidies: Schemes like Pradhan Mantri Awas Yojana (PMAY) offer subsidies on home loan interest rates for eligible homebuyers, particularly first-time buyers and those belonging to economically weaker sections. Research various programs available in your area and explore if you qualify for any financial aid.

Be mindful of your financial goals. While saving for a down payment is crucial, it’s also important to maintain a healthy emergency fund. Aim to have enough saved to cover unexpected expenses without compromising your down payment goals.

Assessing the Impact of Down Payment on Home Affordability

While a larger down payment offers several benefits, it’s important to find the right balance for your financial situation. A very high down payment might deplete your emergency savings or hinder your future financial goals. Here’s how to assess the impact:

- Use Online EMI Calculators: Numerous online EMI calculators are available for home loans in India. These tools allow you to input different down payment amounts and see how they affect your monthly EMI. This helps you determine a comfortable down payment that fits your budget without straining your finances over the long term.

- Finding the Sweet Spot: The ideal down payment amount depends on your individual circumstances. Striking a balance between a lower EMI and the benefits of a larger down payment is key. Consider factors like your financial stability, long-term goals, and risk tolerance when making this decision.

Conclusion

Understanding the intricacies of home loan down payments allows you to make better decisions throughout the home buying process in India. By considering the factors affecting down payment requirements, exploring strategies to save, and assessing affordability, you can approach homeownership with confidence.

ASBL offers a variety of exquisite properties, perfect for starting your new chapter. Let ASBL help you find your dream home, and explore financing options with a lender that best suits your needs.

FAQs

A down payment is the initial sum you pay upfront before securing a home loan. It reduces the loan amount and can lead to lower interest rates and monthly payments (EMIs).

The minimum down payment can vary depending on the loan type, credit score, and property value. It typically ranges from 5% for government schemes to 20% for conventional loans.

Create a budget, explore ways to increase your income, consider using gift funds (if eligible), and research government subsidies to reduce the financial burden.

While a larger down payment offers advantages, finding the right balance is crucial. A very high down payment might deplete your emergency savings. Use online EMI calculators to assess affordability.