Corpus Fund in Apartments 2025: Meaning, Calculation, Sinking Fund Difference & Your Rights

Ever a case where you or your knowns have discussed flat purchase, and then proceeded to discuss fund planning?

During such conversations, you might have come across a term, “corpus fund”. The term might sound difficult to understand, but there’s nothing to be scared of!

Here’s a simple guide to help you understand how corpus fund helps in your apartment purchase. But, before we dive into analysis of its role, we first need to understand what exactly the term means.

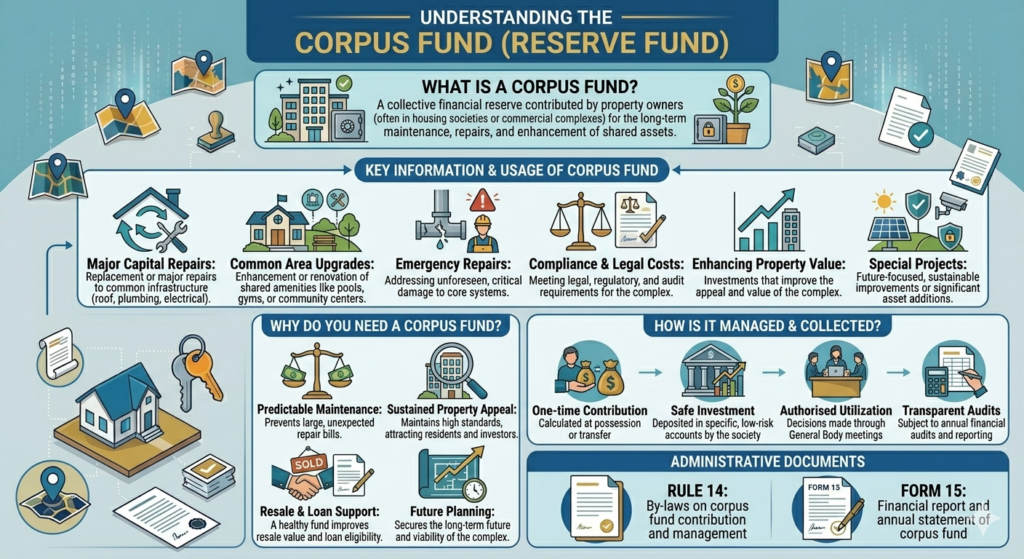

1. What is the Corpus Fund?

To understand in simple terms, think of it in a way that you are making an investment for your building. You make a one-time payment that goes to the bank,this amount is known as Corpus Fund. The original amount never gets used ,and only the interest earned on the amount is used for maintenance purposes.(Source)

What you need to always keep a check of is-

- It’s paid only once, at the time of possession – which implies it’s not to be paid monthly.

- Only the return on investment is used, never the original amount

- Its non-refundable

2. Corpus fund vs monthly maintenance vs sinking fund: Key Differences

- Corpus Fund: The amount paid when you are taking possession of your flat, and its paid only once. It is originally with the builder and later goes to the society’s association, where the interest earned is used for different purposes. It is a kind of fixed deposit.

Example: If there’s a 1000sq ft flat in Kondapur, Hyderabad, and the builder charges Rs. 72 as corpus fund per sq ft,

You pay Rs.72 x 1000 = Rs. 72,000 at the time of possession.

This becomes the principal amount and is in the bank till its given to the society’s association. If the rate of interest is 6% per year, Rs. 4320 goes to the maintenance,while the original amount stays intact.

This amount is witheld by the builder and is passed to AOA, along with all the audited accounts. It’s a mandatory rule under RERA Section-17.

Important: Many builders might delay or partially make the transaction of corpus fund transfer. You need to ask for written proof at the time of flat handover, with details of the bank which is used for holding the amount and proof of complete transfer of corpus amount transferred to AOA.

- Monthly maintenance: A small monthly amount which is collected by the society for building maintenance, and is spent completely, where the amount is mostly dependent on your flat configuration and amenities provided.

Example: 300-unit gated community in Manikonda, Hyderabad,

The society charges Rs. 3.50 per month, per sq ft of the flat.

Considering a 1500 sq ft flat, the amount you need to pay as monthly maintenance is 1500 x Rs. 3.50= Rs. 5250/month.

This amount would be utilised for different purposes like paying the security guards,the cleaning staff,Lift electricity+ AMC,Water + Pump, Club operations,Miscellaneous.

This amount is decided by AOA , which prepares the annual budget, by preparing an estimate of all expenses and planning a budget, which gets discussed in the Annual General Body Meeting and is revised every year.

- Sinking Fund: A major savings chunk which is built with the purpose of large future repairs and replacements, and is built over a time period. The difference between Sinking fund and Corpus Fund is that the principal amount invested is to be spent, as per the requirement.

Example: In 200-unit complex in Gachibowli, say if there are two lifts , each Rs, 15 lakhs and have a life of 15 years, considering the inflation price and the cost of replacement and repairments, in 15 years, Rs. 25 lakh per lift equals Rs. 50 lakhs.

To save Rs. 50 lakhs in 15 years,Rs. 3.33lakhs each year, which amounts to Rs. 1666 per flat per year,is collected as a sinking fund contribution.

The sinking fund covers replacement of lifts,waterproofing of terrace,repainting of the external walls,repairment of underground sump,overhauling of generator, repairs of structures in the system.(Source)

3. How is Corpus Fund calculated: examples of Hyderabad flats

If we talk about how corpus fund is calculated mathematically,

It can be given by the following formula,

Corpus Fund =Rate (per/sq ft) x Area (sq ft)

| Configuration | Typical Locality | Super Built-up Area (sq ft) | Corpus Rate (₹/sq ft) | Corpus Fund Collected (₹) | Annual Interest @ 6.5% (₹) | Monthly Interest Available (₹) | Principal Corpus Status |

|---|---|---|---|---|---|---|---|

| 2 BHK (Budget) | Miyapur / Bachupally | 1,050 | 60 | 63,000 | 4,095 | 341 | Principal remains intact |

| 2 BHK (Mid-Segment) | Kondapur | 1,350 | 72 | 97,200 | 6,318 | 527 | Principal remains intact |

| 3 BHK (Premium) | Gachibowli / Nanakramguda | 1,850 | 100 | 1,85,000 | 12,025 | 1,002 | Principal remains intact |

| 4 BHK (Luxury) | Kokapet / Financial District | 3,200 | 150 | 4,80,000 | 31,200 | 2,600 | Principal remains intact |

4. Legal Framework : What RERA and TAPA say about Corpus Fund

What RERA says about the nature and character of corpus fund

Corpus fund is not the builder’s money,the instance the builder collects it from the buyer,it becomes a legal trust of the flat owners, held by the buyer,where the builder is just a lawful holder, but not the owner.

Secondly, the money collected for the corpus fund is to be treated as a part of the total sum collected from the buyer for a particular project they have invested in, and not as some separate category of money. TSRERA’S FAQ confirms that the corpus fund collected from the buyers is to be a part of the project cost and should be ensured to be deposited in the builder’s chosen account by 70%, the same protected escrow which guards the funds to be used during construction.

In addition to this, RERA sees the creation of AOA and transfer of corpus fund as two sides of the same activity: the two need to happen parallelly. RERA makes it mandatory to form AOA under 3 months central law, where the transactions of corpus start immediately after setting up of AOA legally,which is treated as a violation if the formation of AOA doesn’t happen as per the timeline decided.

RERA’s opinion to what consequences can happen if the builder fails is not explicitly known, the builder owes the AOA an interest SBI MCLR+2% on the amount he had been holding to , for each month of delay. The fact that there could be a case of non-transfer is triggering enough to question the interest liability, while it also provides AOA the right to demand compensation for all actionable loss incurred, for instance, the maintenance work that couldn’t be completed due to unavailability of corpus interest.

What TAPA says about corpus fund

While RERA is mostly focused on the rules and regulations, TAPA is inclined to work on the procedures after the funds reach AOA. TAPA’s positioning holds that once the transaction of the fund happens, the corpus fund becomes a permanent place-holder of the association, legally, which implies that it does not belong to flat owners individually, cannot be distributed among any of the members, and cannot be taken down even if the association is reformed. It is not owned by any of the owners and is a part of the building itself, and this makes it non-refundable, since it belongs to a building as a whole and not a person.

Secondly, in comparison to RERA, TAPA is very specific about what corpus fund can be used for,because of which under Model Bye-Laws under form 5 restrain the funds to be used for: improvisation,alteration of details,repairments, reconstruction and expenditures required specifically for repairing the common areas. It cannot be used for daily expenses nor can it be lent to members, nor can it be used for covering the expenses if there’s a shortage during operational activities.

Furthermore, Rule 7 makes it an obligation that the associations involved in apartment maintenance activities as such should get themselves registered,under either TELANGANA COOPERATIVE SOCIETIES ACT 1964, or the MUTUAL AIDED COOPERATIVE SOCIETIES ACT 1995, the reason falling behind this being, that only a cooperative society gets access to the power of Registrar, for inquiry procedures in case there’s any mismanagement related to funds.

Lastly, Under section 28 of TAPA, any promoter or owner who fails to comply with the Act’s terms and conditions is bound to penalty,which simply implies that a builder who fails to make timely transactions, delays it, makes a partial transfer of the corpus amount or uses the funds other than the building’s maintenance related activities, is liable to punishable offence and can be put into trial under TAPA.

- Is corpus fund refundable when you sell your flat?

To talk about this in straight terms, the Corpus Fund is non-returnable,because the amount belongs to the building and not to someone in specific or to an individual in general, when the flat gets sold, the amount stays with AOA, because what is paid by the buyer at possession is included in the value of the flat, since the buyer takes ownership of maintained building. Neither RERA nor TAPA approves for a refund of corpus amount on selling a flat owner. This holds for all legal positions for all states in India, including Telangana.

Now to understand, why is it non-refundable, here are following three reasons:

Since you already paid the amount from your side, the money is immediately considered to be an asset of AOA, and as per TAPA’s Model Bye-Laws, it is categorised as the permanent corpus fund of the AOA.The money cannot be asked back because it has already been considered a “one-time” investment from your behalf to the building’s maintenance funds.

You can understand it better that, when you paid the corpus amount, you agreed to make a property purchase in a well-maintained building. Considering the maintenance which covers the clean lobbies, well-functioning lifts, workable amenities, the well-maintained common areas, is the main criteria what makes the flat worth of its value when you decide to sell it.

Its not like losing the corpus when you are selling it, rather see it in a way that it had been returning you a better value through a well-maintained building, and the same will keep happening with your potential buyer, which is why you can potentially resell your flat at a higher price in comparison to a flat which is very poorly maintained, since there wasn’t availability of corpus fund.

Lastly, if the corpus was to be returned for every flat, it would evaporate every time a turnover took place. Moreover,the AOA would have no reserves for lift repairments, any major replacements and repairments,or for any emergency situation. Consequently, it would harm the buyers who purchased the flat, ultimately leading to deterioration of the building, and this explains why non-refundability is important for the building to remain structurally fit overall for the upcoming generation of owners.

As a seller, you could follow the following tips:

- Obtain a certificate which clearly states NO DUES from AOA before the sale.

- Ask your builder to give you a clear receipt of the original corpus fund.

- In the sale deed, make sure to include a corpus fund clause clearly.

- Make sure to check the AOA Bye-laws for any resale policies related to corpus.

- If you find that the builder hasn’t transferred the corpus, mention it in the deed.

6) Society handover: how corpus find transfers from Builder to RWA

Under the section 11(4)(e) of RERA 2016, it is the sole responsibility of the builder to maintain the society, until RWA is legally formed, and once RWA takes charge, it becomes foremost for the builders to transfer all maintenance funds with all audits and records.

This also implies that the corpus fund or maintenance charges, is not in any way meant to be the income of the builder, and its mandatory for the builder to have a separate account for deposition of corpus funds and maintenance charges,and the interest earned on these amounts cannot be transferred to their personal account, they need to remain in the same account and get incremented over time.

Step-by-step : How the Corpus Fund Transfer Happens

Step 1: The first step involves formation of RWA by the residents, then electing a committee for management purposes, get themselves registered under the appropriate acts, ensuring that the “Deed of Declaration”is properly registered,and mandatorily open a bank account registered on the behalf of the Association’s name.

Step 2: The next step involves sending a legal notice to the builder requesting for the details of the handover, with clearly mentioned deadlines and approvals pending to be accepted.

Step 3: It’s the duty of the builder to maintain a separate account which must be verified by a Chartered Accountant,which would make it easier for the builder to handover the balance amount details,along with the account statements, which would be well-verified by the CA.

Step 4: A professional inspection is done to check for the collected charges by the builder, and verification of corpus fund transactions to ensure that there would be no future arguments .

Step 5: As per RERA, the transactions and transfer of corpus funds must happen within a time frame of 60 days of RWA registration. Once the RWA is formed, all responsibilities are transferred to the residents instead of being continued by the builder.

Step 6: The RWA must also ensure that they check for society’s sinking fund and previous expenses , dues, security deposits, and AMC contracts and agreements, and ensure that there’s a smooth transfer of agreements to vendors and to the service providers.

7. Red Flags to look for when paying Corpus fund

Before you proceed to paying the corpus fund, here’s a check list you need to go through to ensure no hassle at the end-time of possession.

- Before you sign the documents, make sure you understand all terms and conditions as well the clauses related to the corpus fund, and how much amount the builder wants to collect as a corpus fund.

- The builder’s responsibility is to list down a receipt for showing the corpus fund amount separately, and those which mention the corpus amount as “advance maintenance charges’ or “miscellaneous charges” is to be considered a serious red flag.

- Its the builder’s prime responsibility to hand over the corpus amount collected as well as the interest on it to the society,in either case, if the builder only returns the principal amount and withholds the interest earned,especially at the time when the project is delayed, that becomes a serious matter of financial mishap.

Overall, you need to have a brief understanding of your investments, because your property investments are for once in a lifetime, and you can raise questions to the builder if you feel there are details you need to know or have doubts regarding the funds collected and what you are charged for.